February 5, 2025

.svg)

Thailand’s banking sector demonstrated remarkable resilience in Q3 FY-2024, navigating economic shifts, digital transformation, and evolving customer demands. With a collective revenue growth of 37.7% YoY and rising NPLs, banks must balance profitability with risk management. This analysis focuses on the financial performance of the top Thai banks, assessing revenue trends, profitability, fee-based income, and efficiency while identifying strategic growth opportunities.

Thailand's banking sector showcased impressive resilience and growth in Q3 FY-2024, with leading banks collectively achieving a 37.71% YoY increase in net revenues, climbing from USD 4.1 billion to USD 5.6 billion.

Exhibit 1: Net revenue of top Thailand’s banks

Bangkok Bank

Bangkok Bank demonstrated strong growth, with net revenue rising by 8.78% YoY to USD 1.3 billion in Q3 FY-2024, up from USD 1.2 billion in the same quarter of the previous year. Key growth drivers included a 5.13% increase in interest income—from USD 1.4 billion to USD 1.5 billion—and an 8.78% rise in operating income, growing from USD 1.2 billion to USD 1.3 billion. This performance was fueled by a significant 45.4% surge in investment banking income rising from USD 143 million to USD 208 million.

TMB Thanachart Bank

In contrast, TMB Thanachart Bank reported a 3.3% decline in revenue, dropping from USD 513 million in Q3 FY-2023 to USD 496.1 million in Q3 FY-2024. The primary factor behind this decline was an 18.91% increase in interest expenses and a 10.17% increase in directors’ remuneration.

Key highlights

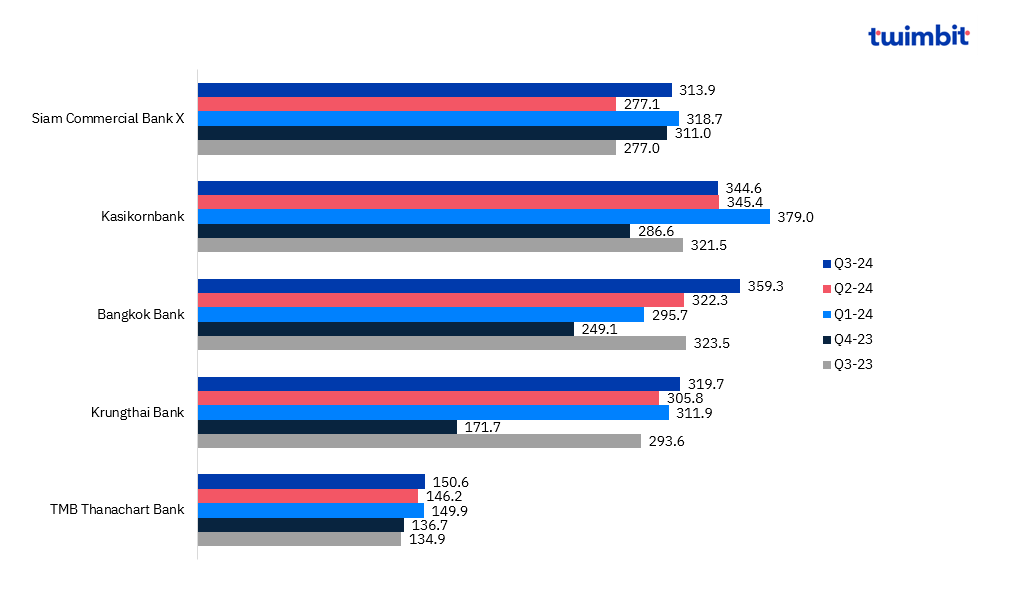

Thailand's leading banks collectively recorded an 11.17% YoY increase in net profits, rising from USD 1.35 billion in Q3 FY-2023 to USD 1.5 billion in Q3 FY-2024.

Exhibit 2: Net profit of top Thailand’s banks

Siam Commercial Bank X

Siam Commercial Bank X (SCBX) delivered an exceptional performance in Q3 FY-2024, reporting a 14.42% YoY increase in net profit, which climbed from USD 275.3 million in Q3 FY-2023 to USD 315.1 million. This impressive growth was primarily driven by a 10.43% YoY reduction in operating expenses.

Key highlights

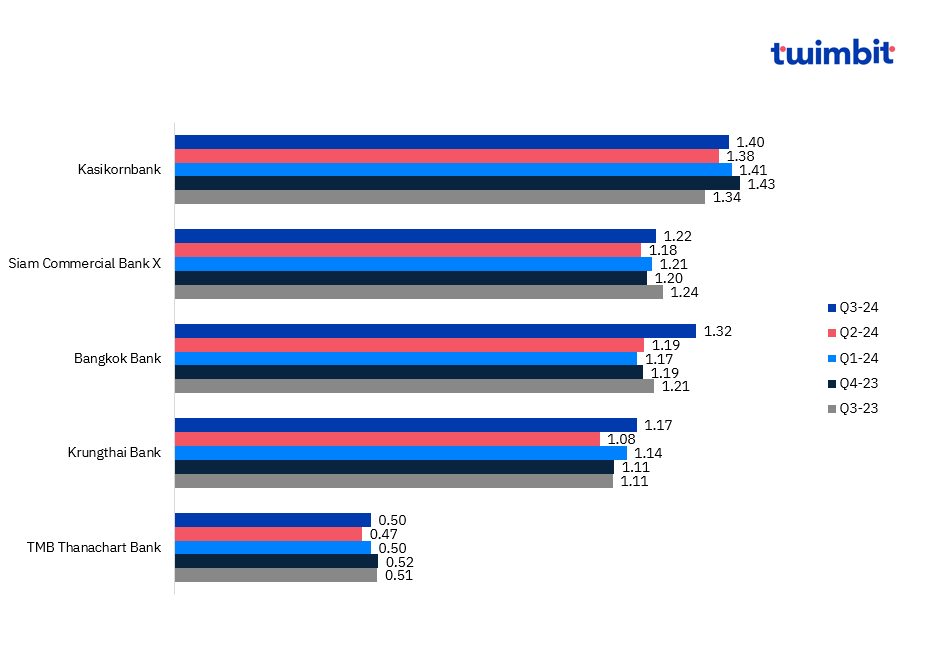

Fee income across Thailand’s leading banks saw an increase of 0.52% YoY, from USD 951.4 million in Q3 FY-2023 to USD 956.4 million in Q3 FY-2024.

Exhibit 3: Fee incomes of the top banks in Thailand

Siam Commercial Bank X

Siam Commercial Bank X (SCBX) delivered an exceptional performance in Q3 FY-2024, reporting a 9.2% YoY increase in fee income, which climbed from USD 223.2 million in Q3 FY-2023 to USD 242.8 million. This growth was primarily fueled by a 34.35% YoY surge in wealth management revenue—from USD 50 million in Q3-23 to USD 67 million in Q3-24—supported by robust fund management, securities, and related services. Additionally, transactional banking income increased by 13.82%, rising from USD 80 million to USD 90.1 million, driven by higher fees, trade finance activities, and FX income.

TMB Thanachart Bank TMB

Thanachart Bank reported a 9.56% YoY decline in fee income for Q3 FY-2024, decreasing from USD 71.3 million in Q3 FY-2023 to USD 64.5 million. This decline was primarily driven by a 6.65% drop in loan-related fees, which fell from USD 3 million to USD 2.8 million, and an 8% decrease in bancassurance fees, declining from USD 29 million to USD 26.7 million.

Key highlights

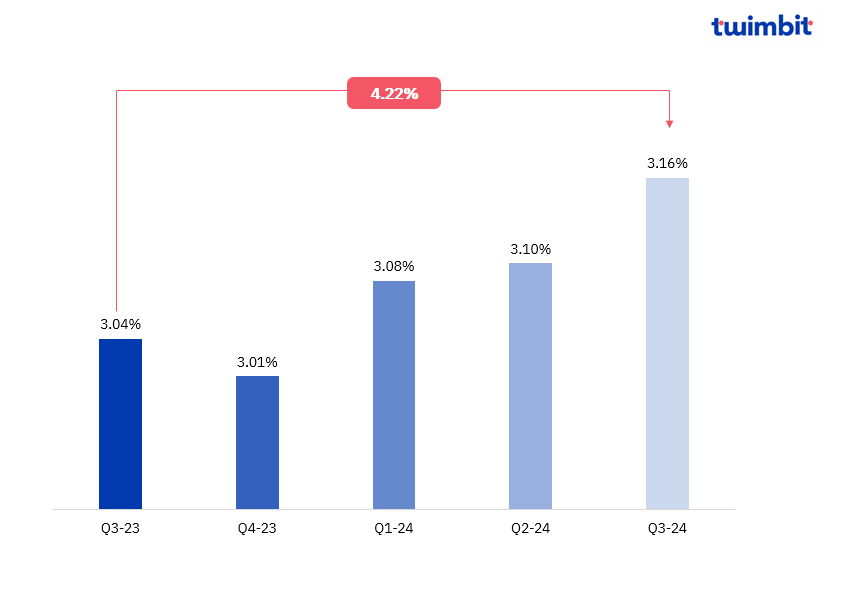

The average NPL ratio across Thailand’s leading banks rose by 4.22% YoY, from 3.04% in Q3 FY-2023 to 3.16% in Q3 FY-2024.

Exhibit 4: Average NPL of the top banks in Thailand

Bangkok Bank

Bangkok Bank recorded a significant increase of 13.33% in its NPL, rising from 3% in Q3 FY-2023 to 3.4% in Q3 FY-2024. This growth was driven by a 6% increase in overdrafts, rising from USD 3.1 billion to USD 3.4 billion, and an 8.34% rise in hire purchase receivables, which grew from USD 121 million to USD 136 million.

Key highlights

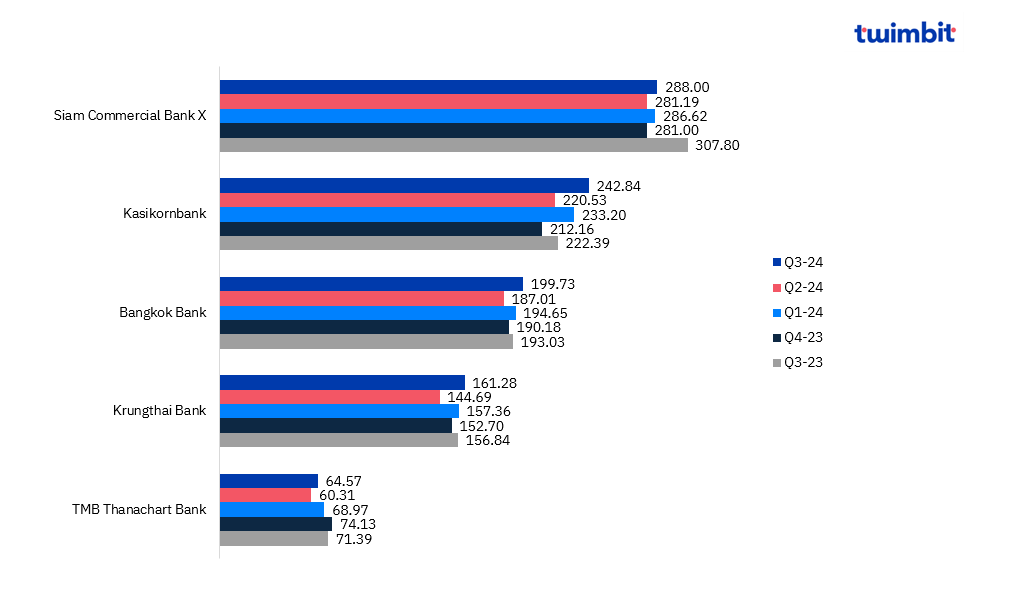

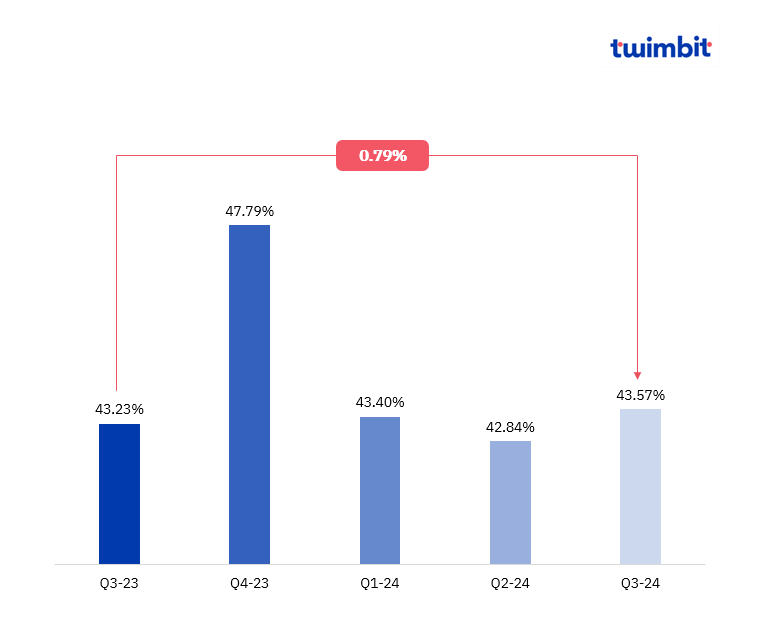

Average cost efficiency across Thailand’s leading banks saw a minor increase of 0.79% YoY, from 43.23% in Q3 FY-2023 to 43.57% in Q3 FY-2024.

Exhibit 5: Average CE of the top banks in Thailand

Bangkok Bank

Bangkok Bank reported a 5.76% YoY increase, rising from 45.1% in Q3 FY-2023 to 47.7% in Q3 FY-2024. This increase was driven by a 9.75% rise in premises and equipment expenses.

Siam Commercial Bank X

Siam Commercial Bank X reported a 3.26% YoY decrease in its cost-to-income ratio, falling from 43% in Q3 FY-2023 to 41.6% in Q3 FY-2024. This decline was primarily driven by a 4.6% increase in interest income.

.jpg)

.svg)

Join 6000+ industry executives who trust us.

Join 6000+ industry executives who trust us.

Subscribe to our newsletter, one trusted by thousands of C-suite executives.

.svg)

.svg)

.svg)

.svg)